.jpeg?lang=en-US&ext=.jpeg)

Find Your Perfect Loan Match

Find Your Perfect Loan Match

This Valentine’s Day, swipe right on homeownership. If you’re a first-time homebuyer, all the mortgage lingo and terminology can be difficult to decipher. Even if you’re not a first-time buyer, it can still seem like your lender is speaking to you in a different language. For example, what exactly does it mean to have a conventional, FHA, USDA or VA, loan? How are they different from each other, and which one is right for you?

It depends. Each loan has pros and cons, depending on your situation.

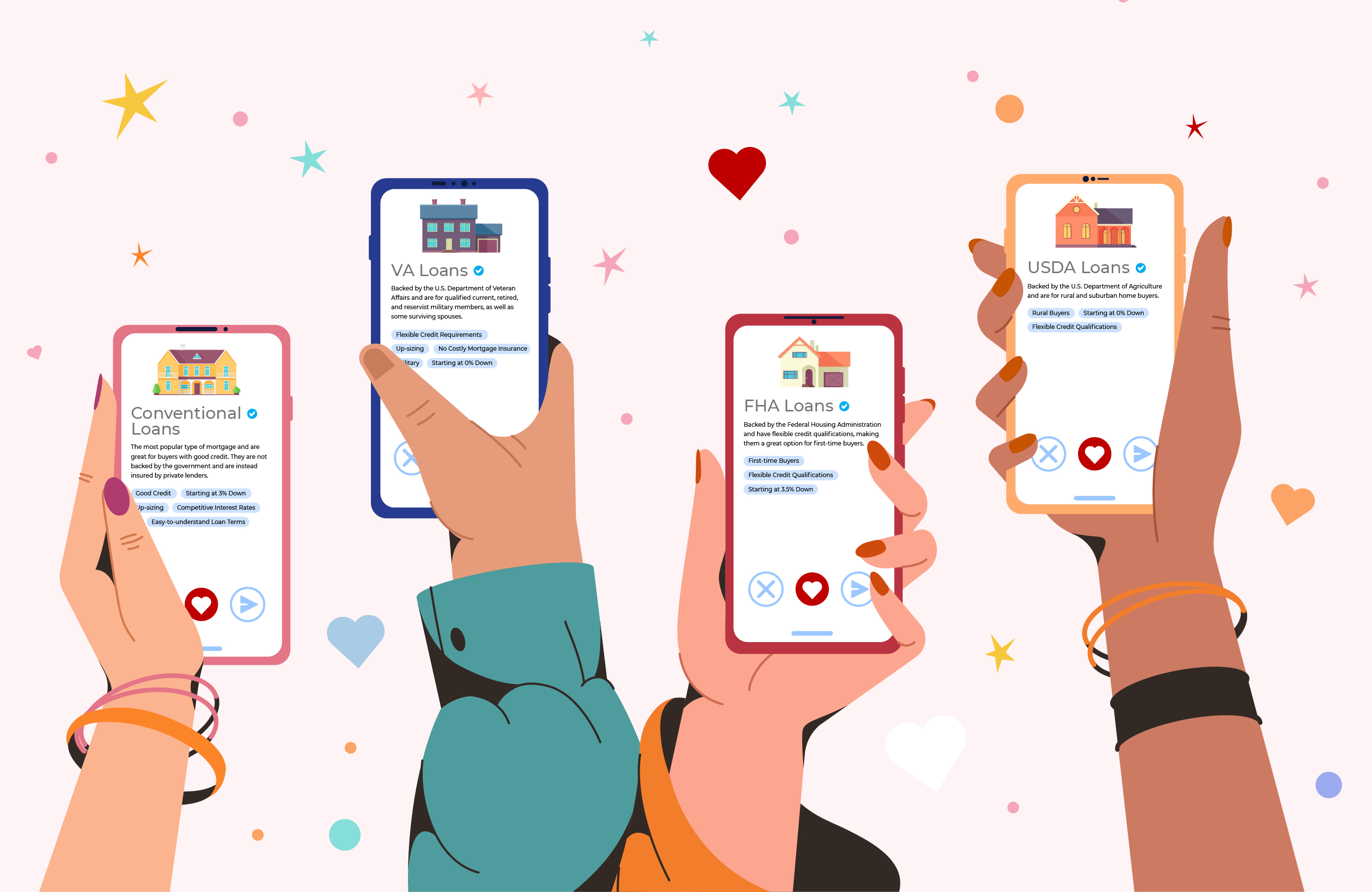

- Conventional loans are the most popular type of mortgage and are great for buyers with good credit. They are not backed by the government and are instead insured by private lenders.

- FHA loans are backed by the Federal Housing Administration and have flexible credit qualifications, making them a great option for first-time buyers.

- USDA loans are backed by the U.S. Department of Agriculture and are for rural and suburban home buyers.

- VA loans are backed by the U.S. Department of Veteran Affairs and are for qualified current, retired, and reservist military members, as well as some surviving spouses.

Down Payment

A down payment is the percentage of your home price that you will pay upfront. Your down payment represents the initial amount of equity—or ownership—that you will have in your home. Coming up with enough cash for a down payment is one of the most common struggles among first-time buyers. But did you know that in most cases, you don’t need to put 20% down on a home, especially your first home? So how much do you need to put down? The answer is different for everyone. Your down payment depends on your lender, your mortgage type, and your financial situation.

Each loan program has its own down payment requirements:

- Conventional loan: Starting at 3% down. The amount may increase depending on your home’s purchase price, the purchase of purchasing the home, your credit score and more.

- FHA loan: Starting at 3.5% down.

- USDA loan: Starting at 0% down.

- VA loan: Starting at 0% down.

Loan Limits

Some mortgages limit the amount that you can borrow. You can still purchase a home that exceeds the loan limit; however, you will need to foot the difference with a down payment.

The 2024 loan limits for single-unit properties are:

- Conventional loans: $766,550, up to $1,149,825.00 in some high-cost areas. Limits set by the Federal Housing Finance Agency (FHFA). For loan limits in your area, click here.

- FHA loans: $498,257, up to $1,149,825.00 in some high-cost areas. Limits set by the Federal Housing Administration (FHA). For loan limits in your area, click here.

- USDA loans: Typically, there are no loan limits.

- VA loans: There is no maximum loan amount, however the VA will use the FHFA’s county loan limits to determine the maximum potential entitlement available for veterans with used or compromised entitlements.

Credit

Your credit can affect where you live, what types of loans you’re eligible for, how much money you can borrow, the interest rate you will pay and might even have an effect on aspects of your personal relationships. Checking your credit score will allow you to know what you’re working with, so you can start updating your credit, if necessary.

Each loan program has its own credit requirements:

- Conventional loans: We typically require a minimum credit score of 640.

- FHA loans: Flexible credit requirements. We typically require a minimum credit score of 620.

- USDA loans: Flexible credit requirements. We typically require a minimum credit score of 640.

- VA loans: Flexible credit requirements. We typically require a minimum credit score of 620.

Did you know that we offer a Credit Enhancement Program? This program is designed to educate and inform customers about their credit and credit scores in order to take advantage of the most beneficial mortgage product.

Interested in learning more about the program? Contact a loan officer on our team to get started.

Private Mortgage Insurance

While these loan programs may not always require a 20% down payment, you will be required to pay private mortgage insurance if you put less than 20% down—unless you are using a VA Loan. The private mortgage insurance will protect the lender on their investment in case you are not able to make your monthly payments, and in some cases can be removed once you reach a certain amount of equity in your home.

The information contained herein (including but not limited to any description of TowneBank Mortgage, its affiliates and its lending programs and products, eligibility criteria, interest rates, fees, and all other loan terms) is subject to change without notice. This is not a commitment to lend. TowneBank Mortgage is a mortgage lender and not a financial advisor, credit repair or consumer credit counseling company. We do not provide investment, tax or legal advice. We do not directly provide services or assistance repairing, modifying, improving or correcting credit.